October 18, 2023

Last quarter, we mentioned that we were likely to see a pause in the market after stellar performance the first half of the year. We expected we may see some “backing & filling”, profit taking, and maybe even as much as a 10% correction. The market was weak in August, and September kept its position as historically the worst month of the year.

We mentioned in July that any corrective action in the 3rd quarter would be healthy even though we said there could be a couple of scary moments. The market was simply ahead of itself through July, and it is healthy longer term to come down a bit and build a better foundation to sustain the next move higher. Over the last three years, September has been down an average of 5-9% depending on the market index. In the last two years the 4th quarter gain averaged 7-11% again, depending on the market index. We expect good 4th quarter performance this year again.

Earnings to the rescue? After a period of earnings recession, earnings expectations are now improving. As a leading indicator, the market looks ahead and starts to price in the return to earnings growth. 3rd quarter earnings growth is expected to be as much as double digits. Obviously, higher earnings at the same valuation means higher stock prices. As of this writing, we are just starting the 3rd quarter earnings season; so far, a high percentage of companies are beating expectations both for revenue and earnings per share. The next couple of weeks will be key as some of the large cap technology stocks will report earnings. We expect solid 3rd quarter earnings, which will likely promote a further increase in earnings expectations going forward.

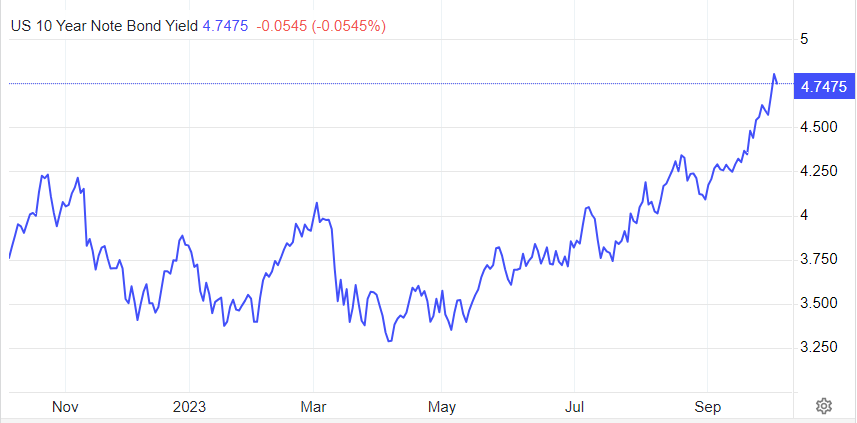

There are a lot of headwinds for the market, but the underlying economic strength has helped the market to be resilient in the face of these concerns. The market has been resilient even in the face of the Israel/Hamas conflict, higher oil prices, strong economic data, which feeds interest rate concerns, and the acceleration of interest rates since May. Interest rates continue to be the primary driver of short term market direction. We would argue that it is not the current interest rate level, but rather the speed at which rates have risen. The chart below shows how fast the 10-year US Treasury rate has moved from May. This was likely caused by supply and demand as the Fed continues to shrink their balance sheet, and the Federal budget has caused the need for much more borrowing by the Government. We believe the Fed is near or at the end of the interest rate tightening cycle and, in fact, the expectations are over 50% for rate cuts by July next year and over 70% by September. We are seeing the potential for slowing economic growth corresponding with a slow but continuing reduction in inflation, which should end the higher interest rate cycle.

We expect solid 3rd quarter earnings, which will likely lead to better market returns into year end. When the S&P500 is up 15% through August, the market has averaged a 4% gain from there to the end of the year. A reminder from last quarter’s commentary as well, when the S&P500 has a first quarter gain following a down year (ten times), the average rest-of-the-year gain was 15.9% with positive returns every time. Also, the last 7 times the Fed cycle of raising rates ended, the market was up an average of 12% a year later.

Going forward, volatility will continue, but with patience, we believe that market will move higher as the interest rate tightening cycle ends, inflation continues to grind lower, earnings rebound, and the economy continues to show growth in spite of all that it has had to endure. For now, good news is sometimes bad news as positive economic news causes short term interest rate concerns. We believe we are near a time when good news is again, good news.

It has been said that human beings make lousy investors. This is due to letting emotions control our decision making. We applaud your patience during short term market stress. Patience has always been rewarded as the market has recovered from market corrections, even bear markets, 100% of the time. The equity market has been the best asset class to meet and far exceed inflation over time.

There has been some concern about the performance of just a handful of stocks skewing index performance. This can also be viewed as a positive in that the majority of stocks are actually undervalued based on historical price to earnings multiples (P/E Ratio). Also, the “magnificent seven”, among other names, are trading at less than a 50% P/E Ratio premium compared to the late 1990’s or the years of the “nifty fifty”. The excitement over AI may create a bubble in time, but we expect based on current valuations, that is years away. In the meantime, AI will likely boost business productivity significantly. This will improve earning and margins and likely lead to a much higher market over the next few years.

We will put out additional commentary as needed, and as always, we thank you for your trust and confidence.

Royal Fund Management